What Exactly Is a Permanent Disability Rating?

A permanent disability rating, often called a PD rating, is a percentage between 0% and 100% that measures the permanent impact your work injury has on your ability to compete in the open labor market. A rating of 100% means you are considered totally and permanently disabled. A rating of 0% means the doctor believes your injury has left no lasting, measurable impairment.

It is crucial to understand that this rating is not simply about your level of pain. While pain is a factor, the rating focuses on your loss of function. It answers the question: How has this injury permanently limited your body’s ability to perform tasks, both at work and in your daily life? The higher the percentage, the greater the compensation you are entitled to receive. We have seen too many hardworking people in Santa Ana accept a low rating because they did not understand that it should account for everything they can no longer do.

The Math Behind the Money: The 2025 California Rating Formula

The PD rating calculation California uses is not simple arithmetic; it is a complex formula with several moving parts. Insurance adjusters know how to manipulate these components to their advantage. Understanding the formula is your first line of defense.

Here is the step-by-step process for the PD rating calculation California uses:

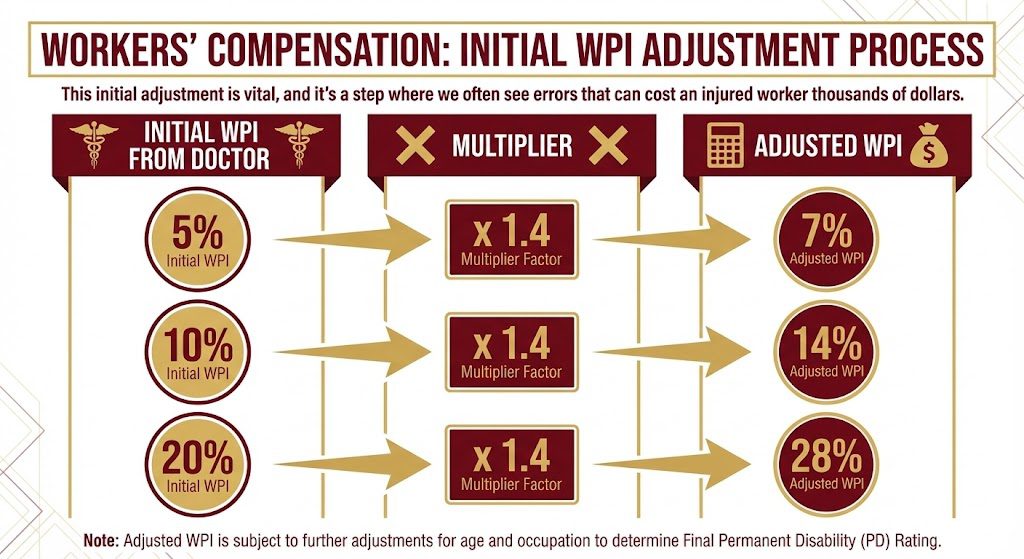

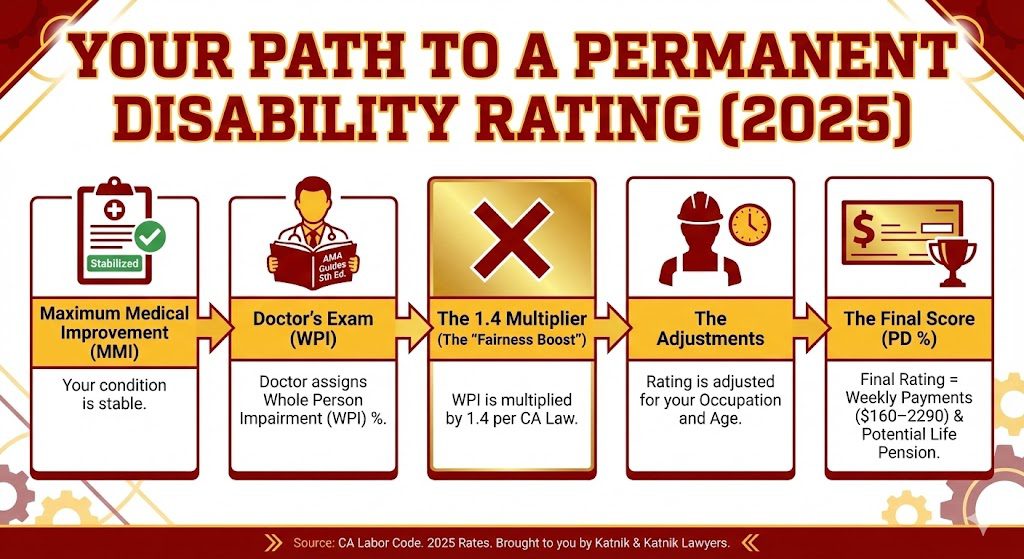

Step 1: Whole Person Impairment (WPI)

The process starts with a doctor assigning a whole person impairment (WPI) percentage. This number is based on the AMA Guides to the Evaluation of Permanent Impairment, 5th Edition. The doctor examines your injury, range of motion, and functional losses to find the closest matching description in this massive book.

For example, a specific type of knee injury might be assigned a 10% WPI. However, a critical law in California requires that this initial WPI number be multiplied by 1.4 before any other adjustments are made. This “1.4 modifier” was enacted to increase fairness in the system.

This initial adjustment is vital, and it’s a step where we often see errors that can cost an injured worker thousands of dollars.

Step 2: The Occupational Variant

Next, the adjusted WPI is modified based on your specific job duties at the time of injury. California’s system recognizes that an injury has a different impact depending on the type of work you do. A hand injury is far more devastating to a Santa Ana construction worker than it is to an office worker.

Every job is assigned an “occupational group number,” which then corresponds to a letter variant (from “A” to “J”). This letter adjusts your rating up or down. A physically demanding job will have a higher variant, increasing your final rating, while a sedentary job may have a lower one.

Step 3: The Age Adjustment

Finally, your age at the time of injury is considered. The system acknowledges that an older worker has less time to recover, adapt, or retrain for a new career. Therefore, older workers receive a slight upward adjustment to their rating, while younger workers receive a slight downward one.

This multi-step formula combines to produce your final permanent disability rating. As you can see, there are multiple points where an insurance company can push for a lower number to save money.

2025 California Permanent Disability Benefit Table

Once your final rating is determined, it corresponds to a specific number of weeks of benefits. The monetary value of each week depends on your average weekly wages at the time of injury, but it is subject to statewide minimums and maximums.

For injuries occurring in 2025, the 2025 workers comp benefits table sets the weekly payment amounts as follows:

For example, a 20% PD rating equates to 70 weeks of benefits. At the maximum 2025 rate of $290 per week, this would total $20,300. In addition, remember that you are entitled to reimbursement for medical travel at the 2025 mileage rate of $0.70 per mile.

The Role of the QME at the Santa Ana WCAB

If you and the insurance company disagree on your PD rating—which happens often—your case may proceed to a Qualified Medical Evaluator (QME). A QME is supposed to be a “neutral” doctor selected from a state-certified list to resolve medical disputes in a workers’ compensation case.

While they are neutral on paper, insurance adjusters are experts at presenting their side of the story to the QME. They will send over medical records that support a lower rating and downplay evidence of your true functional loss. The report this QME writes can make or break your case. All of these proceedings for local workers are handled by the Santa Ana Workers’ Compensation Appeals Board (WCAB), located at 2 MacArthur Place, Suite 600, Santa Ana, CA 92707. Having a skilled Santa Ana workers’ comp lawyer prepare your evidence and arguments for the QME is non-negotiable if you want to secure a fair outcome.

Common Tactics Used to Slash PD Ratings in Orange County

- Insurance carriers are not in the business of paying out claims; they are in the business of generating profits. Their adjusters are trained to use several tactics to reduce your final rating:

- Apportionment: They will argue that a portion of your disability is caused by something other than your work injury, such as a pre-existing condition, a previous injury, or even just the aging process. If successful, they only have to pay for the percentage directly caused by the work injury.

- Ignoring “ADLs”: They will focus only on your ability to do your job and ignore how the injury affects your Activities of Daily Living (ADLs)—things like dressing, bathing, cooking, and sleeping. A proper rating must consider your whole life, not just your work life.

- “Cherry-Picking” Medical Records: They will send the QME a stack of medical records, highlighting every instance where you reported feeling better and burying the reports where you described significant pain and limitations.

How Katnik Law Maximizes Your Award

At Katnik Law, we don’t just process paperwork; we build a case. We bring the grit and determination of the football field to the legal arena. Our team has decades of experience “tackling” insurance carriers in Orange County and fighting back against these tactics. As Certified Specialists in Workers’ Compensation Law, we know the rulebook inside and out.

We maximize your award by:

- Challenging Unfair Apportionment: We fight to prove your work injury is the primary driver of your disability.

- Documenting Your True Impairment: We ensure your doctor and the QME understand the full scope of your functional losses, including your ADLs.

- Controlling the Narrative: We submit our own comprehensive medical summary to the QME to counter the insurance company’s cherry-picked version of your history.

Frequently Asked Questions

How much is a 20% PD rating worth in 2025?

A 20% rating provides 70 weeks of benefits. In 2025, weekly payments range from $160 to a maximum of $290. Therefore, a 20% rating could be worth up to $20,300 in permanent disability benefits, paid out over 70 weeks.

Can I still work if I have a permanent disability rating?

Yes, in most cases. A PD rating under 100% indicates a partial disability. Many injured workers continue to work, sometimes with modifications or in a different role. The rating is meant to compensate you for your lost earning capacity, not necessarily lost wages.

What is the 1.4 modifier in California workers’ comp?

The 1.4 modifier is a factor applied to the Whole Person Impairment (WPI) percentage assigned by the doctor under the AMA Guides. This multiplier, established by Senate Bill 899, effectively increases the starting point for calculating your final permanent disability rating, leading to a more equitable award.

Your Future is Not a Number

The insurance company’s doctor is not the final word on your future. You have the right to challenge a low rating, and you should. The number they assign you will have lasting consequences, and it is essential that it accurately reflects the permanent changes to your life. We understand the profound anxiety and uncertainty that comes with this process, and we are here to provide the support and aggressive advocacy you need.

Your permanent disability rating is more than just a number; it is a recognition of what you have lost. Don’t let an insurance adjuster devalue your experience.

If your rating feels too low, don’t sign anything. Call Katnik Law for a free, confidential rating audit. Let our family help yours secure the justice you deserve.